Tullow "in for a penny..." in Ghana

Tullow "in for a penny..." in Ghana

Deal is accretive vs existing assets and on current metrics, but ties Tullow further into Ghana and the fast declining TEN Field.

*Please read the disclaimers at the base of this report. The author has a short position in the stock. Does not constitute a recommendation to buy or sell the securities mentioned herein. Do your own due diligence.

Tullow has pre-empted Kosmos purchase of Occidental’s Ghana assets, and as a result will raise its stake by 3.4% in Jubilee and in TEN by 7.6%, for approximately $150m, which, at current production rates will raise Tullow’s production by around 5000 barrels of oil a day.

At $75 / barrel long term Brent prices we estimate the value of the purchase at $190m with upside to commodity prices and improvements in performance at Jubilee. On an NPV basis that would equate to around $40m, or approximately 2 pence a share. Our conservative stance is driven largely by our pessimistic outlook on the TEN field, whose performance continues to disappoint according to the latest production figures published by the Ghanaian authorities. We also believe the Ghanaian Revenue Authority will take the opportunity to impose a tax settlement on Tullow as a condition of this pre-emption (recent figures published by Tullow suggest a disputed claim of over $400m).

Interestingly the published figures appear to include October numbers (at bottom, below the total), which, if accurate, show oil production levels of just over 25,000 barrels a day gross at TEN, markedly lower than September (although there may be downtime effects we haven’t accounted for:

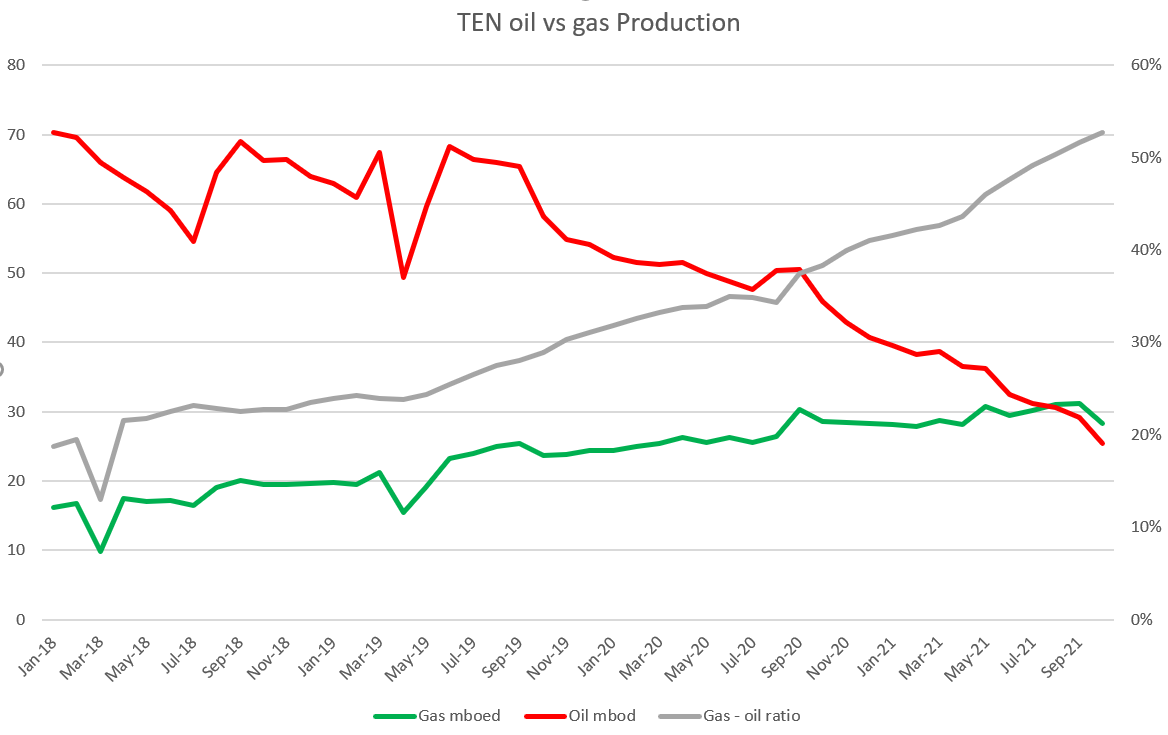

TEN oil production continues to slide, and the field continues to get gassier (gas % on RHS axis):

Rate versus cum analysis for TEN continues to point to not much more than 20 million barrels of economic oil to recover (log rate y axis, 000 bod vs cum oil x axis, 000 barrels), see intersection at x axis of plot extrapolation:

Valuation

Tullow remains burdened by its significant and costly debt balance, which adjusting for the Kosmos pre-emption cost falls close to $2.5 billion of net debt not including the cost of the TEN FPSO (vessel) lease (which would take net debt to over $3 billion). On top of this there is the question of the unsettled Ghana tax claim of over $400m (disputed by Tullow) and the Wisting legal claim of approx $95m. There are also material decommissioning costs in the next few years as well as a negative working capital balance ex the lease cost. Even adjusting for some risking and excluding lease costs Tullow has over $3bn of net liabilities over the next several years while on our numbers we struggle to get above $3.5bn of net asset value, even including some value for exploration, Kenya and probable reserves. On that basis we continue to see better long opportunities elsewhere in the sector, and we remain short the stock vs other sector longs.

DISCLAIMERS

The information contained above is not intended to constitute and should not be construed as investment advice and should not be construed as an offering or a solicitation of an offer to invest in any product or share. It is for personal use and information use only. It should not be relied on in the context of the investment objectives and financial situation of particular needs of any particular person or class of persons, and relevant advice should be obtained before taking any investment decision. The information above has been obtained from sources that we believe to be reliable and accurate at the time of publication, however, we give no warranty of accuracy as to the information or opinions offered above. Opinions given above are given at the time of posting and are subject to change without notice. The value of investments may fluctuate and you may not receive back the amount originally invested. Past performance is not a guarantee of future performance. At any time we may have a position long or short in any given company under discussion