Tullow: Big Bond Bath

Tullow: Big Bond Bath

The real story here is the cancellation of the Bank RBL

While near term sentiment for the equity appears to have improved after the announcement of a mammoth $1.8bn Bond Offering, the clear implication is that the RBL syndicate want to get their money back and exit stage right, leaving bondholders and shareholders carrying the bag.

*Please read the disclaimers at the base of this report. The author has a short position in the stock. Does not constitute a recommendation to buy or sell the securities mentioned herein. Do your own due diligence.

Tullow today announced the launch of a $1.8bn bond deal to pay back its 2021 convertible, its 2022 bond and reduce its bank debt by approx $700m. Effectively its Reserve based Lending facility is being cancelled, and a new facility - a $500m revolving credit facility is being launched.

The details are important because we are within the default curing window for the 31st of March Liquidity Forecast Test. The important language in the Annual Financial Report is as follows: “If the lenders under the RBL facility were to conclude that the information submitted does not fulfil the requirements of the Liquidity Forecast Test and the Group was unable to cure the resulting default by the end of April 2021 there would be an event of default. Such event of default would allow the lenders under the RBL…to cancel the RBL facility…and demand that all outstanding borrowings under the RBL Facility be repaid and/or enforce their existing security rights”

Later it says in the Annual Results that “the Directors believe that, if required, a waiver of such a potential event of default in respect of the Liquidity Forecast Test could be agreed with the lenders under the RBL facility.”

So it seems fair to assume that, given that the plan is to redeem the entire RBL, that the company was unable to secure a waiver of this default event, and therefore is undertaking a last ditch financing to cover its obligations. Part of this is a new RCF of $500m, but it is important to point out that this is not part of the existing facility, but a new facility, with a much reduced borrowing base. As for the $1.8bn, pricing is far from clear, and evidence of pre-marketing is scant. It seems strange to have launched a deal a day before rolling into a long bank holiday weekend in the UK, unless there was some short term urgency driven by the covenant mentioned above.

There are of course other factors. Occidental (Oxy) is rumoured to be selling its stake in the TEN and Jubilee fields (Tullow’s main and only operated assets) for $500m to the Carlyle Group. Oxy owns 24.1% of the Jubilee Field (Tullow 35.5%), and 17% of the TEN field (Tullow 47.2%). The TRACS (reserve auditor) report submitted with the bond launch statement values the gross field values at >3x the rumoured sale value of the Oxy stake to Carlyle. Using the TRACS value splits, the implied valuation of Tullow’s Ghana assets on the Oxy rumoured price tag would be approx $840m. Add TRACS’s value for the remaining Tullow assets (Gabon and Ivory Coast) and you get to $1.1bn vs $2.4bn for the combined new senior issuance, or less than 50c in the dollar. Needless to say, we need to see the final print for the Occidental sale but its not clear there is strong asset backing for this debt, let alone any additional equity value.

We can see this in Kosmos’ SEC disclosure on its Standardized PV-10 for 2021 ($42 Brent) on its 68 million barrels of proved reserves (only 26 of which are claimed as PDP or proved developed producing)

If we take the $364m above, and add $20 a barrel for Brent at $60+, with a drop down incremental net margin of 70%, we could capitalise a further 68 x $20 x 70% x NPV adjustment of say 30% we get to $666m, taking the total to $1030m. Then grossing for Tullow’s working interest gives us $1720m, or approx $2bn adding in the non-operating assets. But even this $2bn is well below the new RCF and bond value of $2.3bn. So even “priced up” 1P values are effectively not covering the debt side of the equation, meaning the debt has to dip heavily into aggressive 2P or probable assumptions before anything is left to equity.

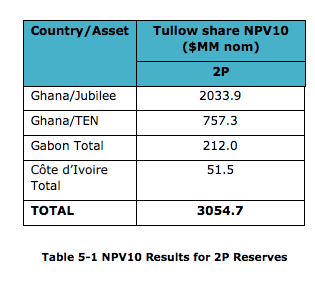

The debt raise is heavily dependent on one asset: in the TRACS report most of Tullow’s NPV value derives from the Jubilee field, despite its higher stake in the TEN field:

These NPV values are based largely on the company’s estimates and on 2P (including probable reserves), so are not as conservative as Kosmos’s valuation. Against our own valuation (see previous note) these figures look high, but even taking them at face value, we can see how dependent Tullow’s valuation is on the Jubilee field, despite what we read in Ghana’s recent petroleum report for 2020:

We know that the asset integrity work on the Jubilee FPSO is only 50% complete in 2020, so much remains to be done even as drilling recommences. Given what we know about TEN and its likely continuing steep decline from our previous work and company disclosure we believe that for the purposes of debt security and equity valuation, Tullow is a one asset company, dependent on Jubilee’s performance, and the performance of a converted FPSO, the KNK, with a problematic history. These are not broad shoulders on which to hang a $1.8bn bond and $500m of bank debt. Little wonder the banking syndicate is cashiering its RBL.

Moreover, there are other factors. The Ghanaian government have a tax claim against Tullow of more than $300m. There is a further legal claim in Norway against Tullow of more than $90m. There is the question of several hundred million of abandonment liabilities, a good proportion of which are due soon. True, the receipts from the Equatorial Guinea sale and Dussufu (Ivory Coast) sale are still outstanding along with a possible contingent payment from Total for the Uganda sale if FID is announced there, however, the point is, there are near term foreseeable outflows, along with risks around gas off-take from both Ghanaian assets.

Additionally there are Ghana specific risks: just take for example what appears to be happening at the Sankofa field operated by ENI which appears to be subject to a forced unitisation with a neighbouring block owned by a “local” Accra based company, Springfield.

In summary, we find the timing of the debt launch intriguing, and believe inference must be drawn from the planned repayment of the RBL in the light of the disclosure around the Liquidity Forecast Test in the Annual Financial Statement. Given the other question marks around Tullow’s assets, the rapidly declining TEN field, and the issues raised above, we remain sceptical of the ability of so much debt to be supported by so little apparent asset value.

As we have already written in our earlier piece (Tullow: Melting Ice-cube), we continue to believe Tullow will require heavily dilutive equity financing even in the event of this bond arrangement being secured. Indeed, while the short term credit trigger may be averted (although that is still not clear), in the long term given the likely high coupon for any bond, Tullow’s financing costs will go up and therefore available cashflow to equity will further diminish, further emasculating any remaining equity value.

DISCLAIMERS

The information contained above is not intended to constitute and should not be construed as investment advice and should not be construed as an offering or a solicitation of an offer to invest in any product or share. It is for personal use and information use only. It should not be relied on in the context of the investment objectives and financial situation of particular needs of any particular person or class of persons, and relevant advice should be obtained before taking any investment decision. The information above has been obtained from sources that we believe to be reliable and accurate at the time of publication, however, we give no warranty of accuracy as to the information or opinions offered above. Opinions given above are given at the time of posting and are subject to change without notice. The value of investments may fluctuate and you may not receive back the amount originally invested. Past performance is not a guarantee of future performance. At any time we may have a position long or short in a given company under discussion.