Serica Energy: Gassing Up

Serica Energy: Gassing Up

Serica is a UK upstream gas producer enjoying the fruits of a tight European gas market

*Please read the disclaimers at the base of this report. The author has a long position in the stock. Does not constitute a recommendation to buy or sell the securities mentioned herein. Do your own due diligence.

Serica is a small cap gas producer that has been hovering at the margins of the UK oil and gas sector for years. Astutely helmed by Tony Craven Walker and CEO Mitch Flegg it has benefitted from the intelligent acquisition of the Rhum (KBR) gas asset from BP and Total. The recent rise in gas prices and a strong balance sheet have put it firmly in the spotlight. With the phase out of many nuclear power stations, and continued shut down of coal fired plants the UK and other European countries are increasingly reliant on gas as baseload for power generation especially when renewables are at the mercy of the weather. As gas prices have risen, Serica has been generating positive net free cashflow, and now in 2022 has complete control of cashflows from the KBR asset. Furthermore, production has recently been augmented by the recent addition of production from the Columbus asset.

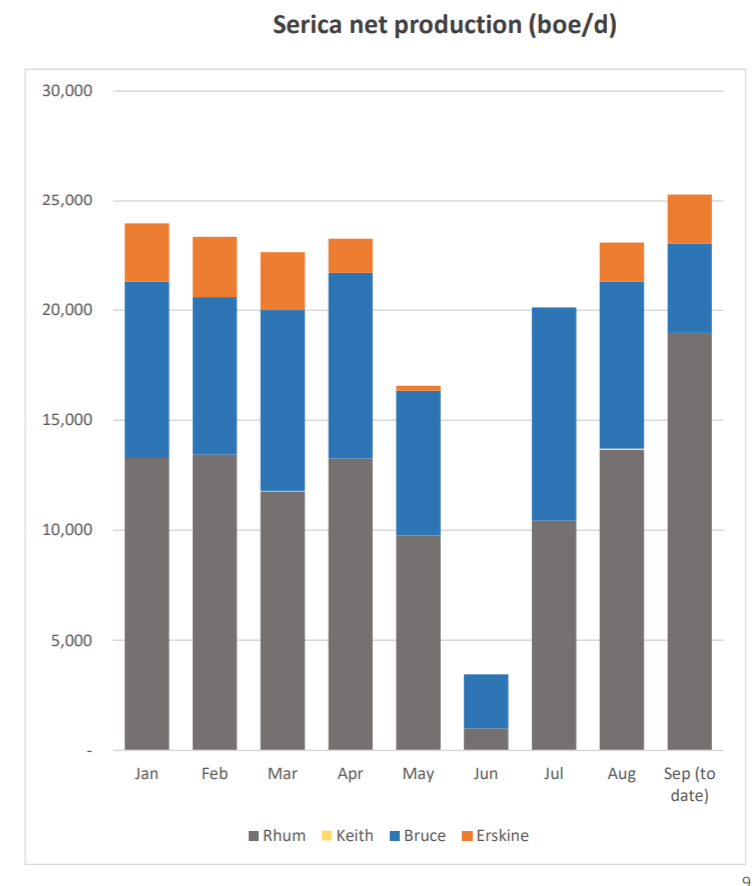

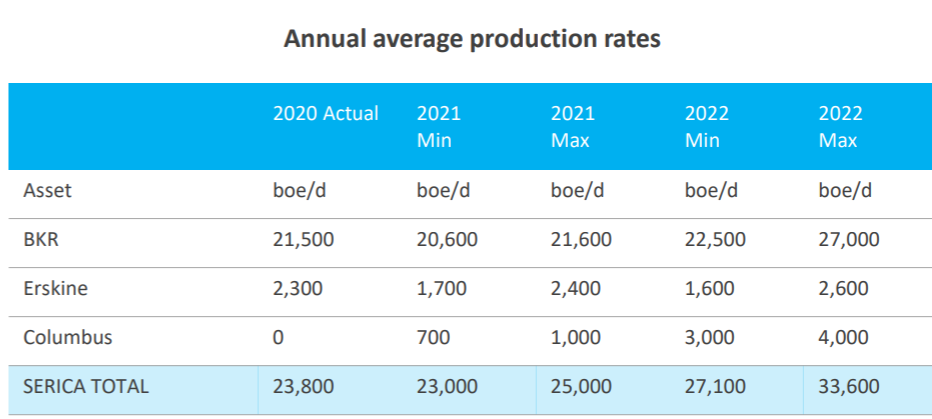

Serica has a market cap of approx $870m at the current share price (240p), with net free cash on the balance sheet of approx $20m (this is the GBP cash balance, converted to dollars, and deducting certain financial and derivative liabilities such as contingent consideration etc). During 2021 it continued to have to share 40% of its net cashflows from its BKR asset as part of its earn-out of its acquisition of those assets in earlier years. That earn-out ended at the end of 2021, and now the company has no obligations to BP or other parties. By November 2021 Serica’s production had risen to 28,500 boe/d (barrels oil equivalent, 85% gas) with Rhums production increase from the R3 well intervention and the tie in of Columbus. For 2022 the company is flagging a broad production range with the mid point at 30,000boe/d.

Between July and November 2021 gas prices more than doubled from 89p per therm to 196p. In December they peaked at 450p per therm before averaging between 150-200p per therm so far in 2022 (February ICE UK gas contract). Future prices for the remainder of this year remain around the 150p per therm level (north of $100 per barrel).

Just running these numbers through a model on a spot basis leads to a combined revenue mix (before hedges) of over $100 a boe driving sales potentially north of $300m in the half year period. Backing out capex, the impact of 35mm therms hedged in H2 (at 39 pence) and the 40% cashflow share on BKR and its still possible to see well north of $100m FCF (free cashflow) in the second half of 2021, potentially taking the cash position to over $200m and the net cash (after deducting debt) position on Serica’s balance sheet to more than $100m

If gas prices remain stubbornly high in 2022 (as they appear to be doing), at over 100p per therm, and with oil prices tracking higher, revenues could be pushing $500m for next year, which post opex could leave $400m of EBITDA, perhaps $340m adjusted for hedges. Take off taxes and capex (say $50m?) and its not hard to imagine FCF generation of a further $140m+ in 2022. That’s nearly a 20% FCF yield.

Now obviously if the government plumps for a windfall tax we could see that FCF shrink, but even with say a move up in taxes of 10% , FCF would still be north of $100m; not as impressive, but still pretty solid.

Admittedly for it to work as an investment you need to be confident in the gas price outlook and the robust competition for LNG from Asia. But with coal and nuclear sources of power generation dwindling in Europe (ex renewables) the supply demand situation seems constructive.

Finally it is worth mentioning the exploration potential going forward with the North Eigg prospect (to be drilled this year), which is adjacent to Rhum and similar in characteristics. The one differentiating facet which might lower the chance of success is that North Eigg is not a four way closure but relies on fault seal against the East Shetland platform, which is obviously a risk, especially for gas. A secondary question concerns the reservoir, assuming they are relying on late Jurassic turbidites and the proximity to the fault (sand bypass risk?). All in all though, still a decent prospect, perhaps a 50-50 shot.

All in all, Serica is a well capitalised pure-play on European gas prices. The management team have delivered so far, and given the potential for significant FCF generation, and building net free cash on the balance sheet, I still believe the risk-reward is favourable.

DISCLAIMERS

The information contained above is not intended to constitute and should not be construed as investment advice and should not be construed as an offering or a solicitation of an offer to invest in any product or share. It is for personal use and information use only. It should not be relied on in the context of the investment objectives and financial situation of particular needs of any particular person or class of persons, and relevant advice should be obtained before taking any investment decision. The information above has been obtained from sources that we believe to be reliable and accurate at the time of publication, however, we give no warranty of accuracy as to the information or opinions offered above. Opinions given above are given at the time of posting and are subject to change without notice. The value of investments may fluctuate and you may not receive back the amount originally invested. Past performance is not a guarantee of future performance. At any time we may have a position long or short in a given company under discussion.

Hi, they said that they have a cash balance of £92m in the H1 results? Where do you get the $20M number from?