Serica Energy: Building Cash

Serica Energy: Building Cash

The company could have over half its market cap in cash in the next few months

*Please read the disclaimers at the base of this report. The author has a long position in the stock. Does not constitute a recommendation to buy or sell the securities mentioned herein. Do your own due diligence.

In our earlier note we laid out the positive investment case for Serica Energy (SQZ LN, SQZ.L). Since the company end of year update, the picture has become a lot clearer. We have seen the addition of over 9000 barrels of oil equivalent (boe = mostly gas) from the R3 (Rhum) well intervention, and the Columbus development (exiting the year at over 3200boed net). December production has almost touched 30,000 boe/d (daily barrels oil equivalent) of which 85% is gas (see investor deck snippet below).

The company had over £218m of cash on its balance sheet at year end (albeit with a sizeable portion held as margin against hedge positions). As hedges mature and the winter price spike subsides, that margin will melt away while substantial bumper revenues from December sales will have hit the company coffers after the close of the year (Serica’s gas marketer tends to hold onto the cash from sales for 30 days or so). UK gas prices averaged 271p per therm in December or approx $212 per barrel of oil equivalent, an unprecedented level, which in turn will see £127m of revenue (gross of costs and hedge & cashflow share offsets) get converted to cash post close of the 2021 accounting year.

From Serica’s updated investor deck:

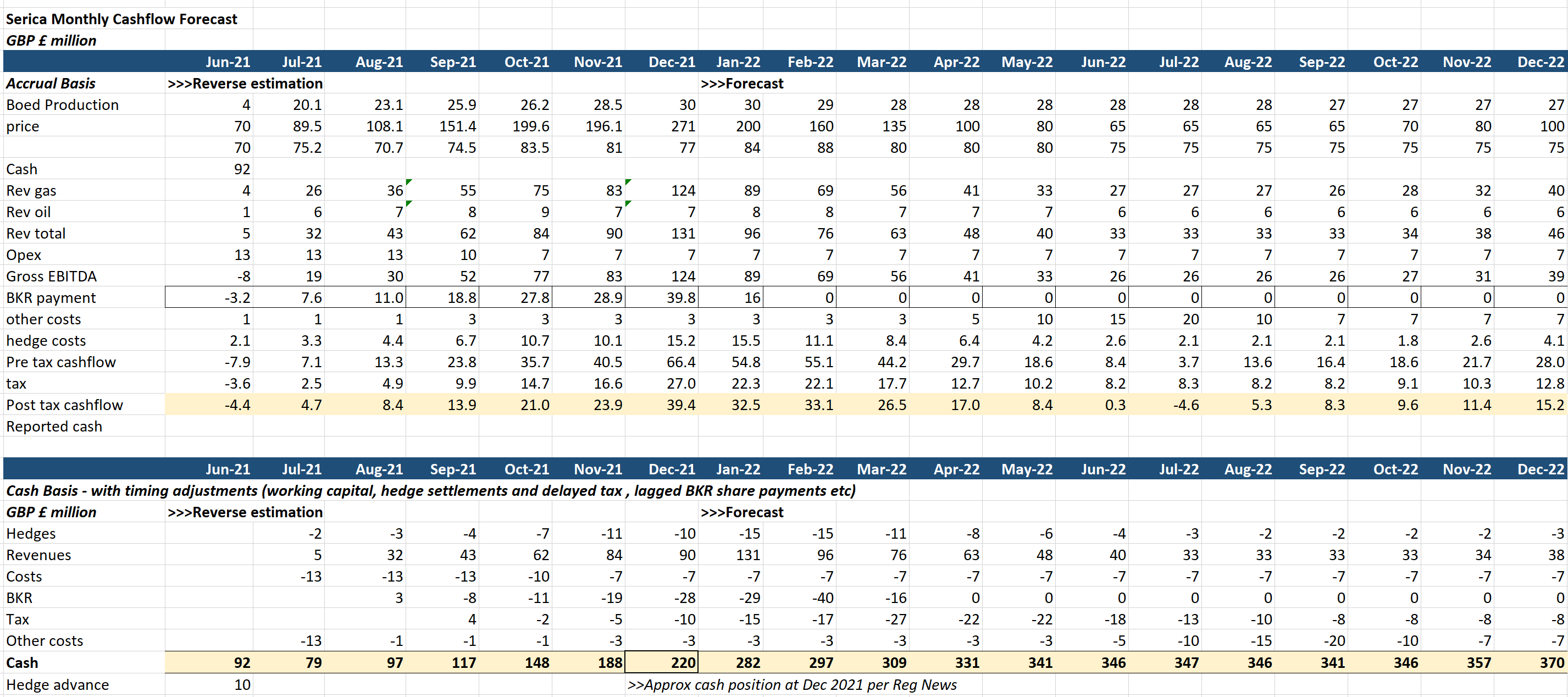

We can see from the above snapshot of the recent investor presentation that the company was producing near 30,000 boe/d in December and in 2022 all of this production will be retained at 100% of cash-flow after the ending of the vendor cash-flow sharing arrangement on the BKR (Bruce, Keith, Rhum) asset. The company has guided for a mid point of 30,000 boe/d of production in 2022, with planned interventions on Bruce and Keith. Given this level of production and the elevated gas prices we have had in January and so far in February (still over 180p per therm or $140/barrel oil equivalent) one would expect cash to mount pretty rapidly on the balance sheet, with cash accruals running at over £30m a month currently and given lags in payments and costs we estimate that balance sheet cash could rise by as much as £80m in January and February alone.

These moves are largely a function of very high revenues from December and January hitting cash balances in January and February, offset in part by lagged partner payments on BKR from November and December and hedge costs. Even if we model out much lower gas prices in the summer (to 65p a therm), we can still envisage net cash generation of around £10m a month in the summer months. With rising gas prices in the following autumn and winter its possible to see the net cash balance exceed £350mm at year end, or over half of the market capitalisation. That would leave approximately £300m of market cap for the ongoing business, comprising say 30,000 boe/d of production, and approx 60mmboe of 2P (proven and probable) reserves.

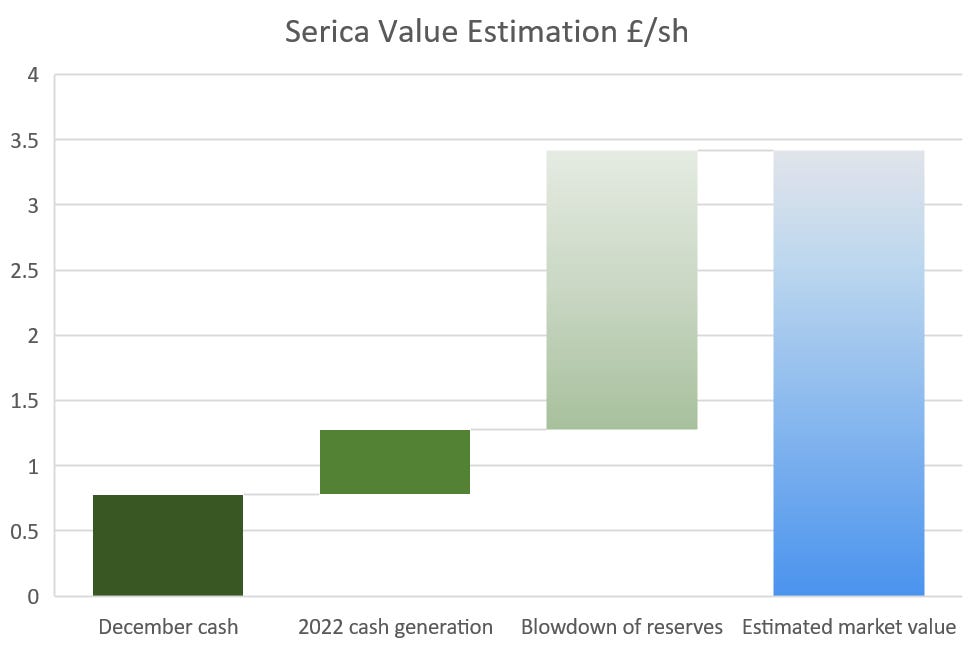

In the waterfall chart below I’ve indicated Serica Energy’s cash journey from year end 2021, adjusting for accruals (ie the lagged payments to the BKR partnership, delayed hedge settlements, tax payments, and December revenues paid in cash 30 days later), and mapped out the step ups in cashflow in 2022. Note that January and February alone, at current prices, could bring in £60m plus of cash (see bottom of appendix for further details, below disclaimers)

If over £350m of the market cap of the company is cash, that leaves the remainder at a valuation of <$14,000 a flowing boe, and only $6.5 per boe of 2P reserves, far lower than peers. Bluntly, the business, assuming this level of near term cash generation, seems extremely attractively valued, in the context of both its UK and global peers (my opinion, not a recommendation to invest). By way of comparison, Tullow Oil has a market cap of £764m or roughly $1bn, and over $2bn of debt: in other words an Enterprise Value (mkt cap plus debt) of $3bn or more. Tullow is producing around 50,000 boe/d, and on that basis is trading on $60,000 a flowing barrel - nearly 4x the value of Serica Energy, or in reserve terms around $12/boe or nearly 2x Serica’s value. Enquest, a North Sea peer, is trading on around $45-50,000 a flowing boe, while larger cap North Sea peer Harbour Energy trades at about $37,000 a flowing boe, and approx $15 a barrel of oil equivalent of 2P reserves. In fact for debt-heavy Harbour, Serica would make a nice tuck-in acquisition, highly accretive on pretty much all metrics even with a 40%+ bid premium, and with the potential to offer “stealth” deleveraging for the acquiror given the extent of the cash generation at Serica is not well documented. Even shale gas producers in the US such as Antero Resources (which achieve far lower gas realisations than Serica) trade more expensively at over $16,000 a flowing barrel, despite earning 80% less for its gas.

Now that Chancellor of the Exchequer Sunak has all but ruled out a windfall tax, I would have thought that debt-heavy North Sea producers will be running the slide rule over increasingly cash-rich Serica, which offers an easy way to both delever and bolt on accretive production and cash-flow, along with near term potential at Bruce and exploration upside at North Eigg which has a decent chance (perhaps 50-50) of adding meaningfully to the reserve base (see appendix).

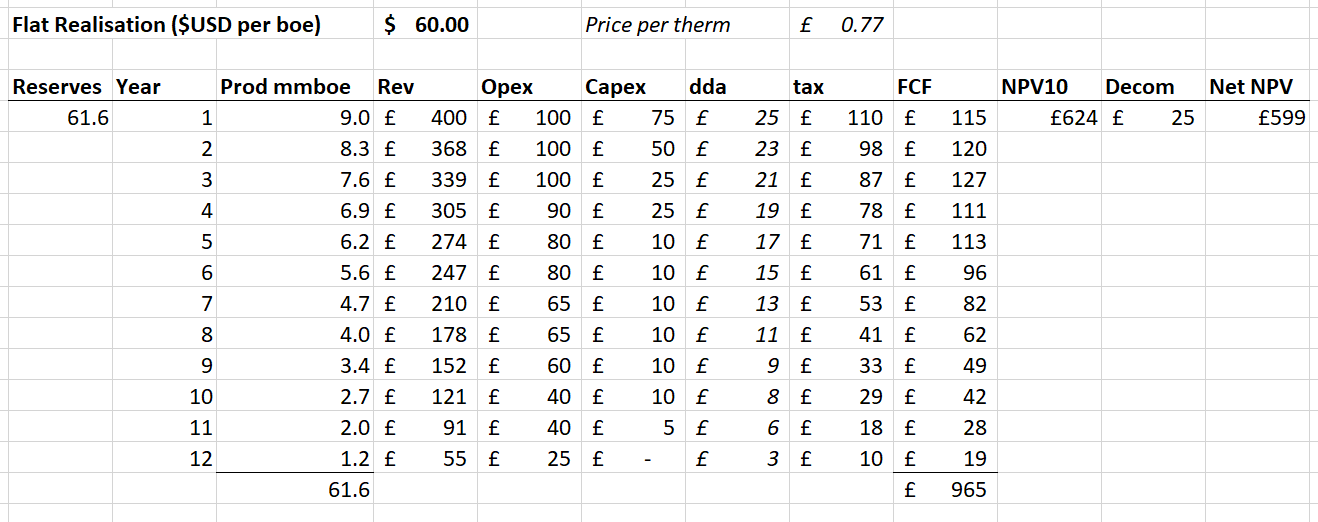

Talking of reserves, at the last update, Serica Energy quoted 2P reserves of 61mmboe. At an average realisation of $60 per boe flat (77p per therm vs 180p currently - implying a lower average per therm gas price given c15% of production is liquids and if oil stays above $60) we get the following blowdown NPV given the above reserve figure.

Assuming that Serica’s net cash position is greater than £350m at year end 2022, and that the company has managed to replace 2P reserves given its investment programme and likely higher price forecasts we would be looking at a market cap target on the basis of the assumptions above of in excess of £920m or £3.41 per share (see estimate value per share below - not an investment recommendation).

As a rough and ready calculation, each 10p move in the average price per therm would add 50p to the share price based on the reserves blowdown above. And obviously much depends on the cash and reserve starting point as we go through 2022. Upside would come from a longer period of super-high gas prices in the UK, or also very high oil prices, as well as exploration success at North Eigg, which would, if commercial, be a fairly low cost tie in to existing infrastructure.

Serica Energy remains a well capitalised, cash rich and (in my opinion) relatively cheap play on a tight European gas market, with a high quality management team helmed by veterans Tony Craven Walker (who sold Monument Oil to Lasmo many years ago), and Mitch Flegg. I continue to own the equity.

DISCLAIMERS

The information contained above is not intended to constitute and should not be construed as investment advice and should not be construed as an offering or a solicitation of an offer to invest in any product or share. It is for personal use and information use only. It should not be relied on in the context of the investment objectives and financial situation of particular needs of any particular person or class of persons, and relevant advice should be obtained before taking any investment decision. The information above has been obtained from sources that we believe to be reliable and accurate at the time of publication, however, we give no warranty of accuracy as to the information or opinions offered above. Opinions given above are given at the time of posting and are subject to change without notice. The value of investments may fluctuate and you may not receive back the amount originally invested. Past performance is not a guarantee of future performance. At any time we may have a position long or short in a given company under discussion. Whilst best efforts have been made, no responsibility is taken for factual errors in analysis or forecasting.

Appendix

North Eigg

The North Eigg prospect (to be drilled this year), is adjacent to Rhum and similar in characteristics. The one differentiating facet which might lower the chance of success is that North Eigg is not a four way closure but relies on fault seal against the East Shetland platform, which is obviously a risk, especially for gas. A secondary question concerns the reservoir, assuming they are relying on late Jurassic turbidites and the proximity to the fault (sand bypass risk?). All in all though, still a decent prospect, perhaps a 50-50 shot.

Monthly Cash Accrual/forecast 2022e

Numbers above are based on monthly modelling below for cash forecasting - (obviously subject to human error and forecasting/estimation bias).

Good morning - I thought the 8th Feb 2022 update you did on Serica Energy was an excellent note. It was detailed, informative with easy to understand number crunching. Most important of all is - you have been proved correct - congratulations. in light of the Government's Windfall Tax

and the update from Serica last week, I wondered if you had any plans to update your 8th Feb 2022 note . I was trying to find a way to subscribe , but failed so any help you could provide would be appreciated. Thank you and keep up the good work.....John Reilly

ps - I have been a shareholder of Serica since its original listing.