Serica Energy

*Please read the disclaimers at the base of this report. The author has a long position in the stock. Does not constitute a recommendation to buy or sell the securities mentioned herein. Do your own due diligence.

Ticker: SQZ.L, SQZ LN

Recently Kistos PLC, a listed acquisition vehicle owning gas production in the Dutch offshore sector, opportunistically submitted a bid for Serica that values the company at currently just over £4 a share, comprising Kistos PLC stock (0.4 sh) and 213p cash, a chunk of which would be distributed from Serica’s growing cash pile. That offer, on our analysis, (and we can assume that of Serica’s board), materially undervalues Serica given the current macro environment, and we agree with Serica management’s decision to turn the offer down. Not surprising as we can plausibly model Serica at around 1x EV/EBITDA on current macro trends for net year, and <3-4x EV/FCF or a free cashflow yield on enterprise value of over 25% in 2023.

Since we last wrote about the company in February, the gas market has been upended by the war in Ukraine, sanctions against Russia, and Russia’s response in throttling back exports to Europe via NordStream 1. As a result, European storage levels remain extremely challenged and futures prices going into the winter suggest in excess of $300 a barrel of oil equivalent for gas.

Serica has not been free of of drama, with an operational hiccup early in the spring bringing down Rhum production due to a defective piece of subsea equipment, which impacted its exposure to extremely high gas prices in March 2022. In spite of that, cash has continued to pile up on the balance sheet, with production soon returning to full capacity, and gas prices remaining highly elevated, despite a disconnect between NBP (UK spot prices) and the Dutch TTF price driven by LNG cargoes landing in the UK, temporarily filling limited UK storage capacity at import terminals.

Recently that cash build (£396m by end of May 2022 per management) has brought bidders out of the closet, with Andrew Austin’s acquisition vehicle Kistos making two bids for the company which have so far been rejected by Serica’s board. The Kistos bid appears opportunistic given the continued recent cash build at Serica (inferred from the continuing spike in gas prices), the relative premium valuation for Kistos (see below) and also because of the mismatch between Dutch gas prices and UK gas prices which has now largely closed.

We have also had the announcement of the Energy Profits Levy in late May, which has spooked some investors: in fact, given Serica’s investment programme (including the drilling of the North Eigg prospect in H2 2022), the enhanced allowances on offer for capital investment offset a good proportion of that increased taxation.

So where do we stand today? Well on my monthly cashflow forecast the company is set to generate a meaningful ramp in cash balances going through to year end, with a high likelihood of hitting more than a £500m cash balance at year end. Our year end forecast assumes a spike in December 2022 of gas prices to crisis level peaks but a more benign scenario through the autumn, along with lower oil prices. This and the fact we assume delayed tax payments through the summer make £500m+ seem more than achievable by year end:

The final row above is our estimated month end cash balance for the firm.

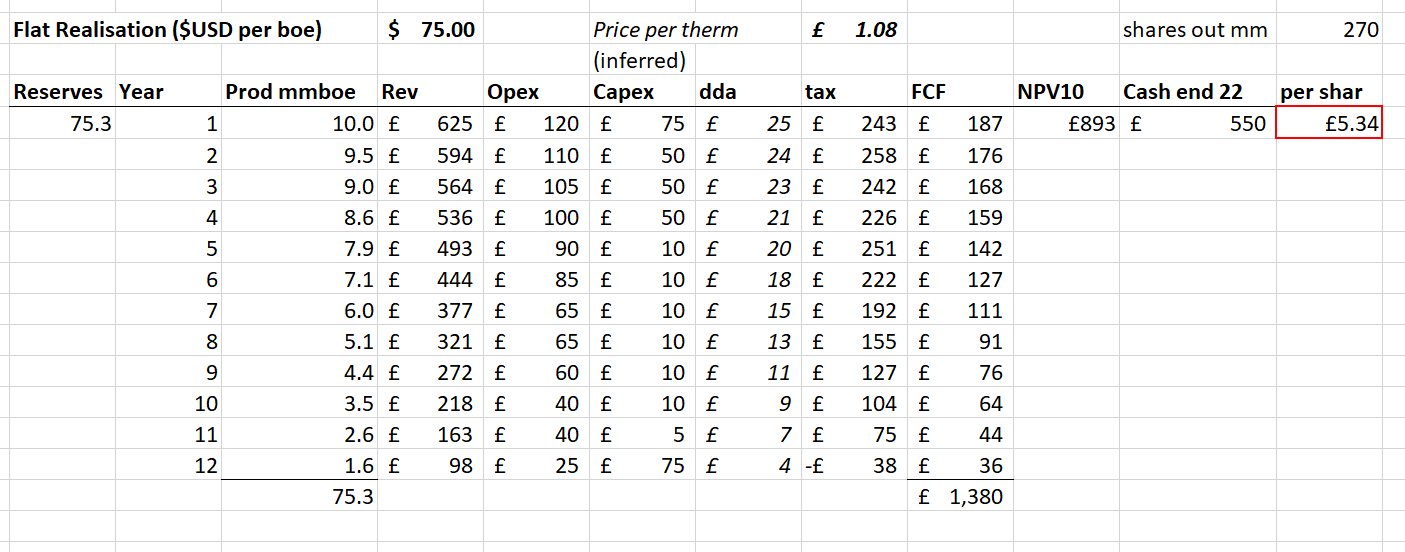

If we take this number and then estimate further out, we end up with the following resource blowdown value (below). Here, I have assumed a limited reserve increase at year end reflecting the well interventions at Bruce and Rhum but without material resource adds from the North Eigg exploration well (which is currently being drilled and could offer the opportunity to double reserves near existing infrastructure). I have factored only a 15 million boe uplift to reserves in my blowdown below as a consequence of this year’s drilling and investment, which I believe is conservative.

I think the above £5.00+ valuation underplays the investment opportunity given the current exploration programme (eg North Eigg), and further potential nearfield resource capture, alongside the tax benefits of capital investment (which are minimised in the above “blow-down” scenario (effectively a 12 year liquidation assumption). The P50 pre drill case for North Eigg is approx 60mmboe, which if achieved, could double Serica’s current reserve base. We should find out the results of that well in October.

The main risks to the stock, outside major unexpected operational failure, are obviously commodity prices, but an oil price forecast of $75 (well below where we are), and effective gas parity pricing to oil at just over £1 a therm, seem conservative to me given gas prices well in excess of £3 a therm currently. And anyway, investment is a relative game - there are plenty of dearer investments in the sector discounting much higher values and subject to the double leverage effect of higher operational costs and high indebtedness (see table below). All this makes me continue to be happy holding the stock unless shareholders offered something that gives me a healthy premium to the valuation sketched out above. I don’t believe a mix of Kistos’s stock and Serica’s cash will give me that on the terms outlined so far.

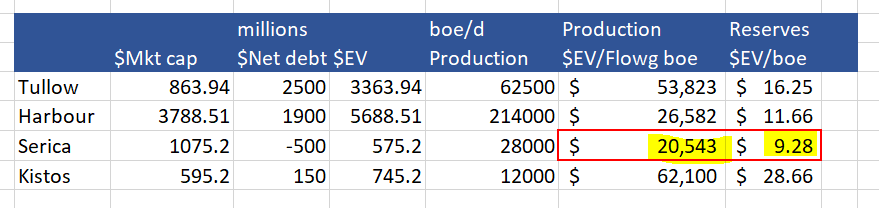

As for Kistos, on a pro-forma basis post completion of the Greater Laggan asset purchase their EV (or enterprise value) is approx $750m vs Serica’s estimated EV of $575m (using assumed net cash of $500m at the half year point). That is in spite of Serica’s production being over 100% higher than Kistos and with approx 3x the reserve base.

For a quick rough and ready comparison I’ve put the following comparison table below together where I’ve put together two metrics, EV (Enterprise value) per flowing barrel of oil equivalent, and EV per barrel equivalent of 2P (proved and probable) reserves. Prices are as at 5th August 2022 and debt levels are a guesstimate/extrapolation from year end levels (Dec 2021).

Of the listed UK E&Ps, Serica really is the standout here. No wonder Kistos is offering its apparently dear (to my eyes) equity for its stock.

I continue to maintain a long position in Serica and will not be voting for any deal from Kistos as currently proposed.

DISCLAIMERS

The information contained above is not intended to constitute and should not be construed as investment advice and should not be construed as an offering or a solicitation of an offer to invest in any product or share. It is for personal use and information use only. It should not be relied on in the context of the investment objectives and financial situation of particular needs of any particular person or class of persons, and relevant advice should be obtained before taking any investment decision. The information above has been obtained from sources that we believe to be reliable and accurate at the time of publication, however, we give no warranty of accuracy as to the information or opinions offered above. Opinions given above are given at the time of posting and are subject to change without notice. The value of investments may fluctuate and you may not receive back the amount originally invested. Past performance is not a guarantee of future performance. At any time we may have a position long or short in a given company under discussion. Whilst best efforts have been made, no responsibility is taken for factual errors in analysis or forecasting.

What about ENQ and HUR, which look very cheap?