Hurricane Energy: Brent to the rescue?

Hurricane Energy: Brent to the rescue?

The company has clung on, paying down the majority of its outstanding debt, but how long can Lancaster hold up?

*Please read the disclaimers at the base of this report. The author has a short position in the stock. Does not constitute a recommendation to buy or sell the securities mentioned herein. Do your own due diligence.

Hurricane Energy has defied expectations since I last wrote on it, with equity holders avoiding a debt refinancing with a court process that was seemingly bungled by management and the bond holders. High oil prices have allowed the company to channel its monthly receipts into a tender for the 2022 convertibles at an attractive discount, and the company has followed up with further purchases at far more modest discounts. There is the tantalising prospect of the company reaching positive net cash by the time the Aoka Mizu FPSO needs to be handed back to Bluewater this sumnmer (unless a flexible extension can be agreed).

And yet. Before going into full reverse ferret mode and pondering whether Hurricane is about to “moon”, lets inject a dose of reality. As things stand Hurricane’s platform has to be demobilised in June-July. The higher oil price environment presumably makes a floater like the Aoka Mizu with its EPS system more attractive to other upstream operators keen to cash in on the stronger environment. Bluewater may thus have alternatives. And it is not going to be cheap to move towards abandonment and decommissioning - earlier reports in 2017 (RPS) suggested $45m plus.

Meanwhile, other potential costs are identifiable. Hurricane generated 200,000 tonnes of CO2 in 2020. UK ETS prices have gone through the roof in 2021 - without free allocations, which Hurricane doesn’t appear to have, the company could be on the hook for over $16m per annum of carbon credits (at $80 per tonne). And that number will likely go up a lot, give production at Hurricane is set to get gassier as the gas comes out of solution with production below the bubble point.

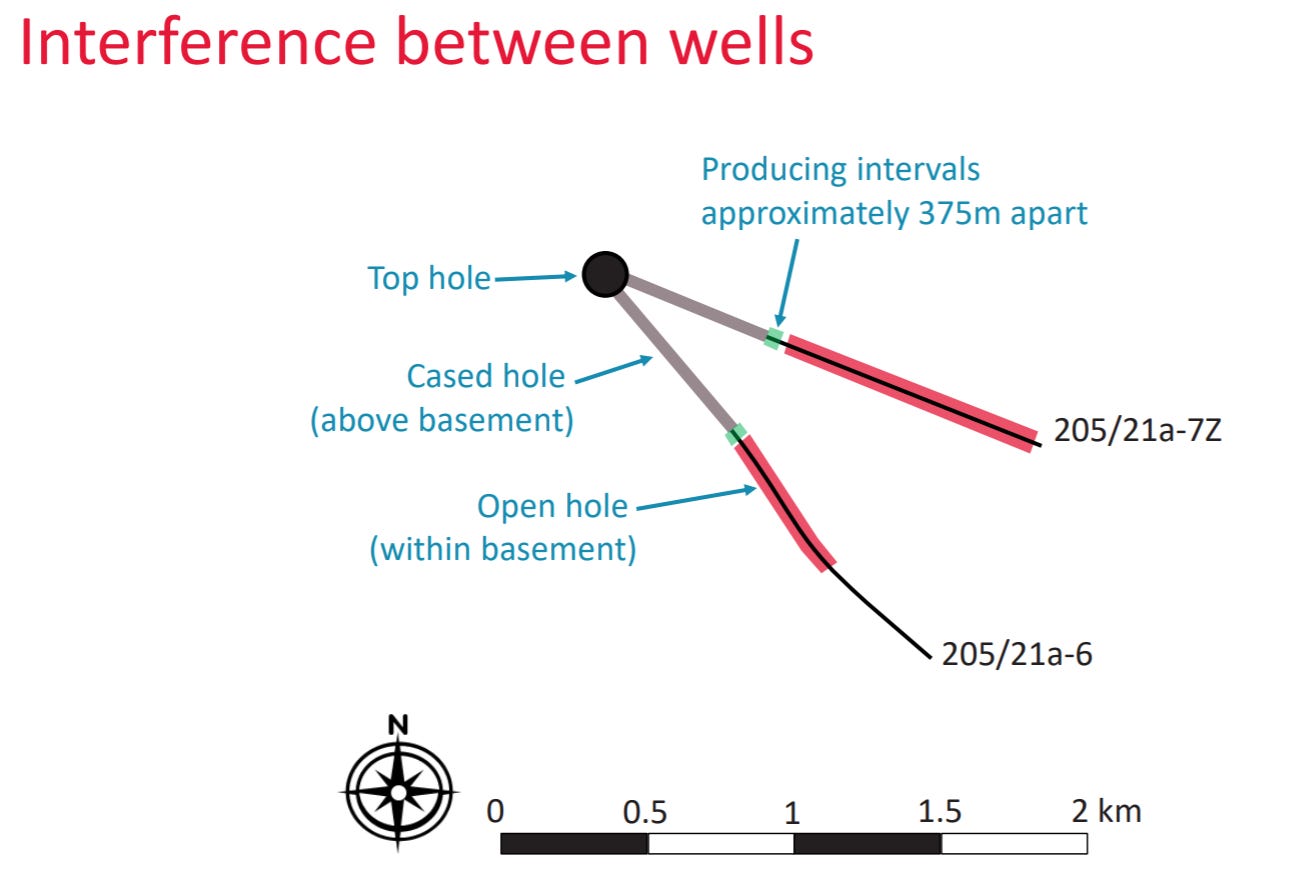

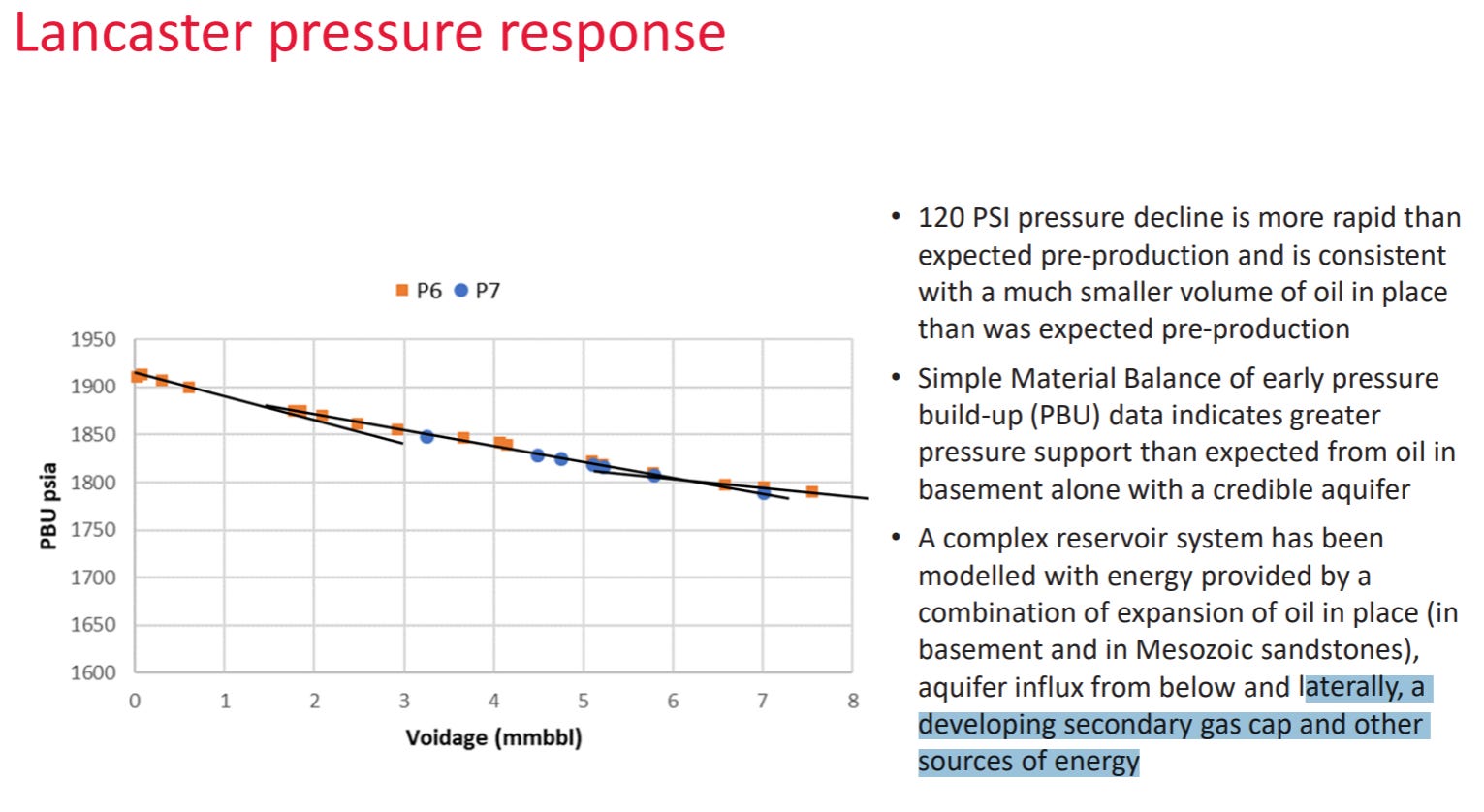

And that is the key point: the last producing well, the P6 well, has now dropped below bubble point pressure of roughly 1600psi. Monthly declines seem to have nudged up to 5% and the water cut is approach 40%. It is only a matter of time before a gas cap builds and starts to interfere with the well perforations which produce the oil, depending on where those perforations are. So far we are only a few weeks into below bubble point production, but if a gas cap forms its a fair assessment that gas could enter the well bore out of solution.

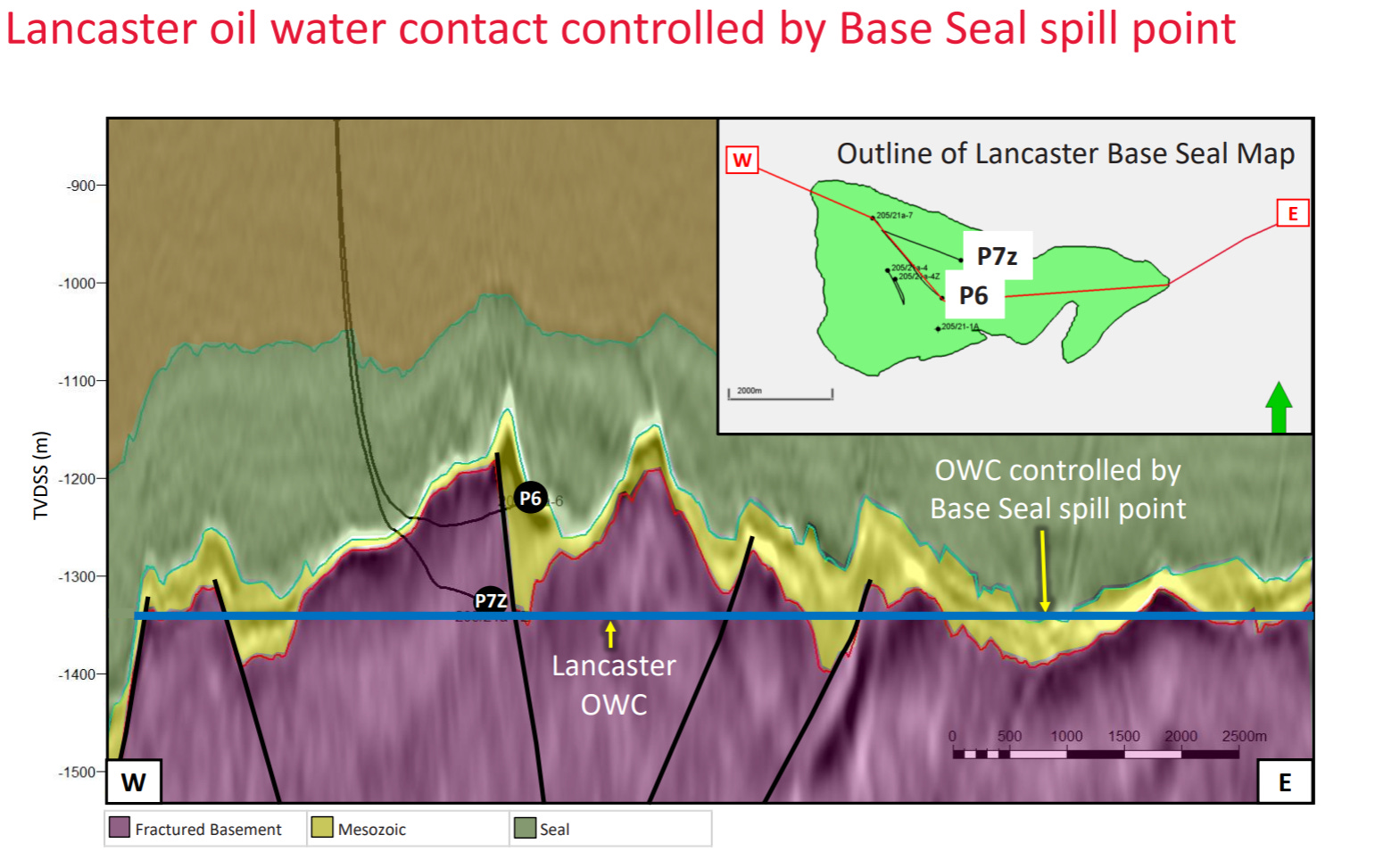

Part of the problem is where the P6 well was originally drilled, as you can see from this 2020 schematic from the company. The well, which has its end bit sealed off is horizontally positioned fairly high up in the oil column, which is fine from a water contact point of view (although water cut is now approaching 40%) but less good if you are envisaging a developing gas cap (from a historic Hurricane presentation):

See the P6 trajectory above in this cutaway? Not much room for a burgeoning gas cap to develop without encroaching on the wellbore. Interesting to note too that the wellbore is open-hole, not cased in the fractured basement zone, which means gas contact at any part of the wellbore can encroach into the well (from a historic Hurricane presentation):

The thin black wick at the end of the P6 is (I assume) plugged and sealed as you can see on the schematic that it cuts through a fault line. It is possible that there are super-conduits of fractures cutting through the bore which may attract water from below, and increasingly going forward, gas pushing down from above - a sort of inverse-coning situation.

If we take a “tank” view of the area above the P6 well bounded by the wellbore and the seal with the fault on the right we can see that there is not a huge area “above” the bore hole where it is horizontal, compared with the basement rock below the borehole. In other words, it wouldn’t take much of a developing gas cap to fill it. Note that in a 2020 presentation, Hurricane management already mentioned a developing gas cap (see highlighted text) at much higher pressure levels than current (1600psi):

As the pressure falls further, the gas cap should build further, and with pressure lower around the bore this may concentrate there, so it would not be prudent for investors to bank their hopes on relatively flat production (or shallow decline) from here. Obviously the bull case is that the gas cap acts as a piston to push oil out in a gas/oil/water sandwich but in practice it is not as simple as that and the “formation high” positioning of the P6 wellbore puts that theory into question.

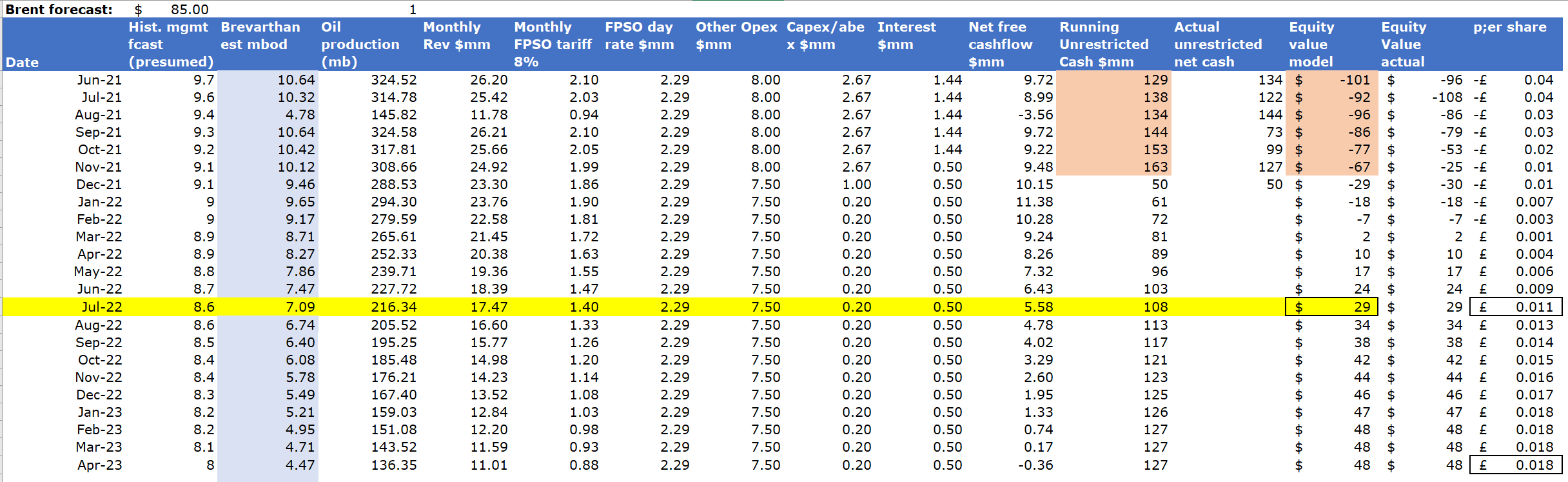

Granted, the well is currently “cash-flowing” at between $8-10m net per month (of costs, capex, interest, opex and G&A) at current oil prices. At the end of December net debt looks to be around the $30m level using reported cash numbers against the remaining convertible debt ($50mm vs approx $80mm of debt). In theory three months of sustained production at these prices could wipe out the debt, and six months could leave the company with a net cash position of $30mm or more. But given what we have seen of decline and the steady march of water cut is that really likely? Production would only have to halve from here to eliminate free cashflow and we only need the example of the P7z well (without a gas cap) to see how water cut above mid 40% impacts production of oil. It seems very plausible given the risk on gas and indeed water cut (adding 1% per month) that production will continue to decline, possibly rapidly.

Meanwhile increasing gas production from gas in the wellbore raises flaring risks (OGA consent) and UK ETS risks given current prices of >$80 per tonne of CO2. ETS costs are now material even with current flaring (200kt of CO2 pa or more) and will become much more material if that level increases as I expect it should. So costs will be rising at the same time production is falling.

Finally even if we just accept a (highly unlikely in our opinion) low rate of decline (c3% per month) as a “high case”, what does that leave us with. Well if we adduce that Bluewater consent to allow the Aoka Mizu to continue on current terms we would hit economic limits sometime in 2023 with net free cash (debt free) at maybe $95mm ($85 Brent). The current market cap is around $120mm. Our indicative cashflow model is below where we model a conservative decline rate of 5% mom from February 2022.

We can only assume then that investors see more value in Hurricane than in the value of current production. Perhaps the tax losses have some value, however hiving down an asset like Lancaster and using its tax losses is not a straightforward question: the losses are not really portable without the asset as a producing entity, and the company owning the asset itself would have to be the acquiror rather than the acquiree. While these issues are not insurmountable, its hard to believe that these losses are worth a large number of cents on the dollar if acquired even in some sort of reverse transaction, though we are happy to stand corrected.

Our base case is rapid further decline of the P6 well and higher levels of (expensive) flaring given gas encroachment of the well, with a material risk that Bluewater (the FPSO owner) walk away in the summer of 2022 when the current contract expires. We also note that Crystal Amber (which has successfully litigated on behalf of shareholders last year), which owns just south of 30% of the shares, has recently lost a wind-up vote and as a result is now a net liquidator of its assets pending any plan it announces.

We remain short the equity.

DISCLAIMERS

The information contained above is not intended to constitute and should not be construed as investment advice and should not be construed as an offering or a solicitation of an offer to invest in any product or share. It is for personal use and information use only. It should not be relied on in the context of the investment objectives and financial situation of particular needs of any particular person or class of persons, and relevant advice should be obtained before taking any investment decision. The information above has been obtained from sources that we believe to be reliable and accurate at the time of publication, however, we give no warranty of accuracy as to the information or opinions offered above. Opinions given above are given at the time of posting and are subject to change without notice. The value of investments may fluctuate and you may not receive back the amount originally invested. Past performance is not a guarantee of future performance. At any time we may have a position long or short in any given company under discussion